On this page

What's next

Earn a high-yield savings rate with JG Wentworth Debt Relief

By late 2025, household debt in the U.S. had climbed to a staggering $18.59 trillion. [1] Alongside this, Experian reports that the average American held $104,755 in debt as of mid-2025. [2] People take on debt for many reasons, ranging from student loans to fund education to auto loans that support everyday travel, and these obligations can build up over time.

To explore why people borrow money, we surveyed 1,011 U.S. adults about the reasons they have taken on personal debt throughout their lives. This includes credit cards, personal loans or using overdrafts. The findings reveal recurring themes of financial pressure and urgency, with many respondents reporting that they borrowed to cover unexpected or emergency expenses.

Key findings:

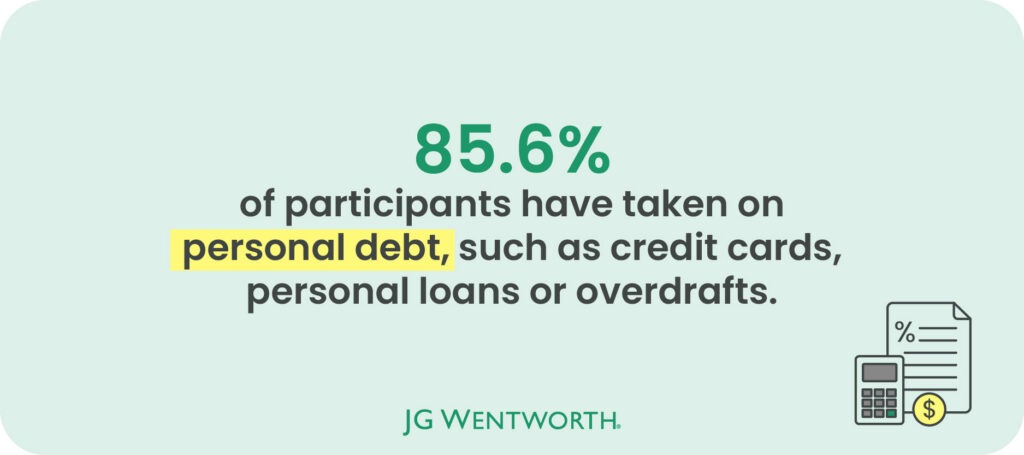

- 85.6% of participants have taken on personal debt, such as credit cards, personal loans or overdrafts at some point in their lives.

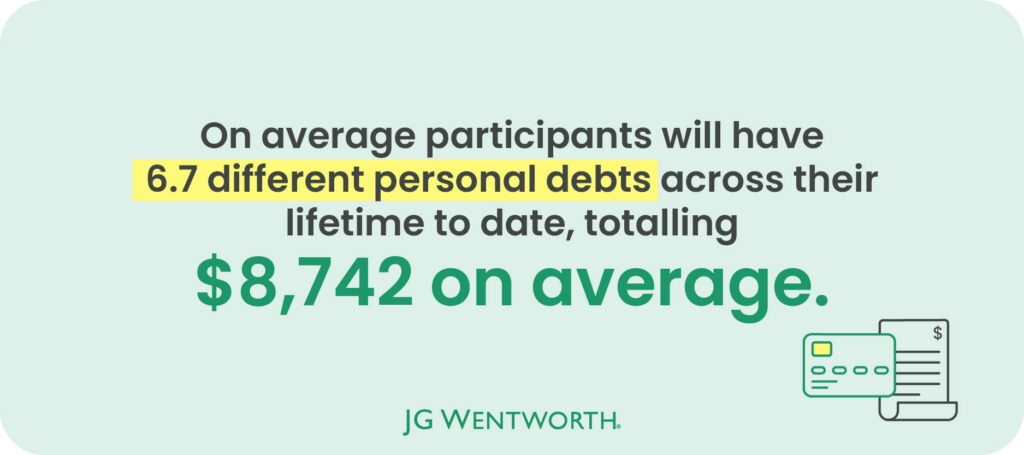

- The average American will have 7 different personal debts in their lifetime totalling $8,742 on average.

- The most common reason for taking on personal debt is to cover unexpected emergency expenses (31.4%).

- This is followed by medical expenses (27.9%) and day-to-day living expenses (26.4%).

- Reducing spending (43.5%), increasing income (35.8%), and help from friends and family (26.6%) were the most common methods to overcome the debt.

- Over three quarters (75.6%) admitted to missing or delaying payments because of their personal debt situation.

- Over half (51%) admitted that their personal debt had significantly affected their ability to cover basic living expenses, such as rent, utilities or groceries.

How common is debt in America?

The research shows that borrowing is a common part of financial life for most people, with 85.6% of participants saying they have taken on personal debt at some point, whether through credit cards, personal loans, or overdrafts.

Summary

- U.S. household debt reached $18.59 trillion by late 2025, with the average American holding $104,755 in personal debt as of mid-2025, according to Experian.

- The most common reason Americans take on personal debt is unexpected emergency expenses such as car or home repairs, cited by 31.4% of survey respondents.

- Medical expenses rank second at 27.9%, reflecting the average U.S. household medical debt burden of $10,570 reported in 2025.

Just 14.4% of respondents said they had never taken on this type of debt. However, most of this group (65.1%) still use credit products, choosing to pay their balances in full each month to avoid accumulating debt. Careful budgeting was cited by 55.5% as the main reason they have stayed debt-free, and many expressed confidence (38.4%) that they could continue to avoid debt even in the event of a major unexpected expense.

On average participants hold 4.3 types of personal debt at the same time

On average, respondents reported holding 4.3 personal debts at the same time at their peak, rising to 6.7 in total across their lifetime to date. When asked about the total value of debt accumulated, participants reported an average of $8,742, highlighting how multiple smaller debts can quickly add up over time.

The most common reasons for getting into debt

The primary aim of the study was to uncover the most common reasons Americans take on personal debt, including credit card balances, personal loans, and overdraft usage.

The findings reveal that emergencies are the leading driver of borrowing, with nearly a third of participants (31.4%) citing unexpected expenses such as car or home repairs. Research suggests that emergency car repairs could range from $3,000 to $7,000 to cover issues such as transmission or engine replacement, [3] while home repairs, such as plumbing problems, a leaking roof or HVAC failures could cost as much as $2,000 to $4,000. [3]

The most common reasons for getting into debt

| Rank | Reason for getting into debt | Percentage of participants |

|---|---|---|

| 1 | Emergency expenses (i.e. car or home repairs) | 31.40% |

| 2 | Medical expenses | 27.90% |

| 3 | Day-to-day living expenses | 26.40% |

| 4 | Education costs | 26.20% |

| 5 | Job loss or income reduction | 23.40% |

| 6 | Cost of housing | 22.50% |

| 7 | Financially supporting a partner | 20.60% |

| 8 | Unnecessary spending | 20.50% |

| 9 | Financially supporting a family member | 19.50% |

| 10 | Having a child | 18.30% |

| 11 | Marriage (i.e. wedding costs) | 17.90% |

| 12 | Financially supporting a friend | 14.50% |

| 13 | Having another child | 11.60% |

| 14 | Divorce | 5.40% |

Medical expenses were cited as the second most common reason for falling into debt. In 2025, the average household was reported to hold $10,570 in medical debt, [4] and because medical emergencies can affect anyone at any time, it is perhaps unsurprising that these costs are pushing many Americans into borrowing.

The third most common reason for taking on personal debt was the rising cost of everyday living expenses. Data from the Bureau of Labor Statistics shows that prices for essential goods and services, including food (2.9%), medical care services (3.9%), and electricity (6.3%), increased in the 12 months prior to January 2026. [5] This, combined with an increase in the unemployment rate from 3.7% in January 2024 to 4.3% in January 2026 [6] may have contributed to a growing reliance on debt to cover basic necessities.

The least common reasons for taking on debt were divorce (5.4%), having an additional child (11.6%), or providing financial support to a friend (14.5%). Despite the fact that over 1.8 million Americans divorced in 2023, [7] and the average cost of a divorce is around $11,300, [8] relatively few respondents reported taking on debt because of it.

Over four in five (83.2%) are still paying off their personal debts today

When asked if they were still paying off personal debts, a striking 83.2% of participants said they were, leaving just 16.8% who had fully cleared their balances. On average, respondents still owed $7,354, which is only $1,388 less than the total amount they had originally borrowed, showing how debt can persist long after it is first taken on.

The most effective ways to clear personal debt

| Rank | Used to help pay off debt | Percentage of participants no longer paying off debt |

|---|---|---|

| 1 | Making more than the minimum payment | 32.40% |

| 2 | Reducing social or leisure spending | 26.20% |

| 3T | Paying off smallest balances first | 23.40% |

| 3T | Reducing discretionary spending | 23.40% |

| 3T | Paying off highest-interest debt first | 23.40% |

| 6 | Freelancing or contract work | 22.10% |

| 7 | Overtime at an existing job | 21.40% |

| 8 | Tracking balances regularly | 20.70% |

| 9 | Canceling subscriptions | 20.00% |

| 10T | Changing jobs for higher pay | 19.30% |

| 10T | Taking on a second job | 19.30% |

| 10T | Switching to cheaper brands | 19.30% |

| 13 | Selling unwanted items | 18.60% |

| 14 | Consolidating debts into one loan | 17.90% |

| 15 | Family or friends providing financial help | 16.60% |

| 16 | Freezing or closing credit accounts | 13.10% |

| 17 | Negotiating interest rates with lenders | 12.40% |

| 18T | Declaring bankruptcy | 11.70% |

| 18T | Monetizing a hobby | 11.70% |

| 20 | Seeking debt advice | 10.30% |

*Participants could select multiple options.

On the other hand, participants reported that some strategies were less effective in reducing their personal debt. Seeking professional debt advice helped only 10.3%, while monetizing a hobby and declaring bankruptcy were each cited by 11.7% as useful in paying down debt.

The most common methods to reduce personal debt

The survey asked participants which methods they were using to reduce or clear their personal debt. The most common approach was simply cutting back on spending, chosen by 43.5% of respondents. This was followed by increasing income (35.8%), seeking help from friends or family (26.6%), and setting up a payment plan with a lender (26.4%).

| Rank | Method | Percentage of participants |

|---|---|---|

| 1 | Reduced spending | 43.50% |

| 2 | Increased income | 35.80% |

| 3 | Help from family or friends | 26.60% |

| 4 | Payment plan with lender | 26.40% |

| 5 | Debt consolidation | 23.10% |

| 6 | Professional financial advice | 20% |

| 7 | Refinancing | 19% |

| 8 | Bankruptcy | 15% |

*Participants could select multiple options.

On the other hand, methods such as declaring bankruptcy (15%), refinancing (19%), or seeking professional financial advice (20%) were less commonly used. Despite bankruptcy being a less popular strategy for reducing or clearing debt, research from 2024 shows that bankruptcy filings in the U.S. rose by 14.2% compared with the previous year. [9] Our recent research found that California is the best U.S. state for financial second chances, while New Jersey offers the most challenging conditions for getting back on your feet.

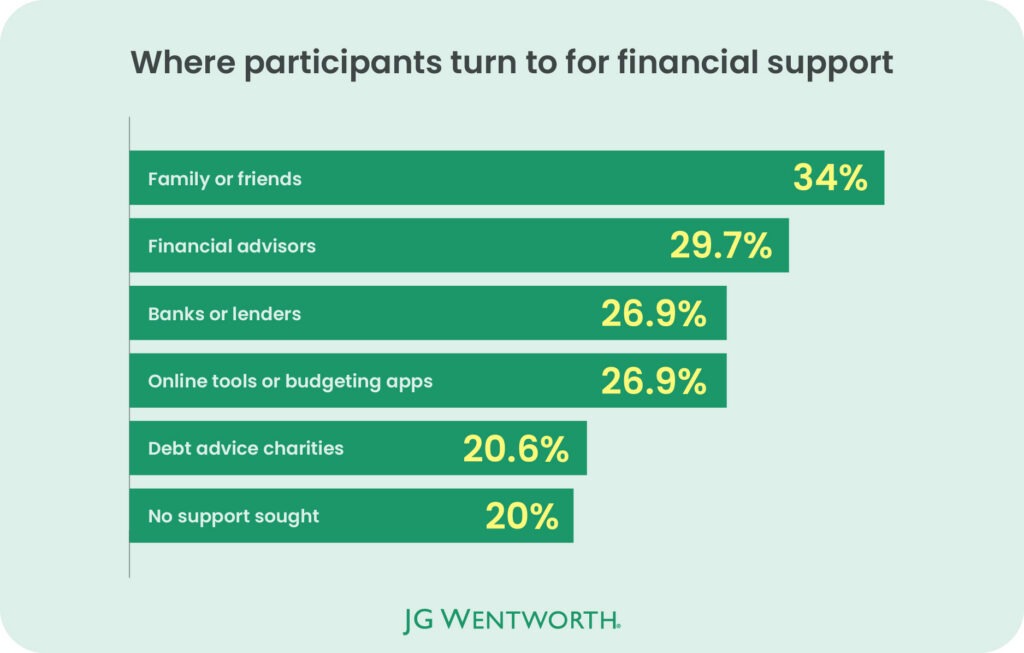

Almost one in five (19.6%) turn to friends and family for financial support

In addition to traditional methods for reducing debt, the survey asked participants about the types of support they have turned to. Over a third (34%) said they relied on friends or family for help managing their personal debt. While only 20% reported seeking professional advice, popular forms of support included financial advisors (29.7%), banks or lenders (26.9%), and online tools or budgeting apps (26.9%).

In addition, participants were asked which formal debt solutions they had used for managing their personal debt. The most common approach was a debt management plan, used by 38.4% of respondents. This was followed by debt consolidation loans (34%) and debt settlement (27.5%), otherwise known as debt resolution or debt relief.

Debt solutions include a range of strategies designed to reduce or clear debt outside of the formal bankruptcy process. The most common types of debt relief include debt consolidation, debt negotiation, debt settlement, or credit counseling. It’s important to note that each of these methods work differently, and each person’s individual financial circumstances will dictate which method is most effective for them.

The impact of personal debt

The survey explored the lasting effects of personal debt and how it continues to influence participants’ financial decisions.Over one in ten (11.1%) say the debt did not help the issues they were facing

When asked whether the personal debt they had taken on helped resolve the financial issue they were facing at the time, 58.5% of participants said it completely solved the problem. Another 30.4% said it was somewhat helpful but did not fully resolve the issue. However, 7.3% admitted that taking on the debt actually made their financial situation worse, and 3.8% said it had no real impact either way. A 2025 Bankrate study found that taking on too much credit card debt is one of the biggest financial regrets for Americans, [10] highlighting the importance of carefully considering any borrowing before using it to address financial challenges. Our own research echoed this as 76.6% said they regret taking on their personal debts.Personal debt is impacting basic living expenses for almost nine in ten (86.7%)

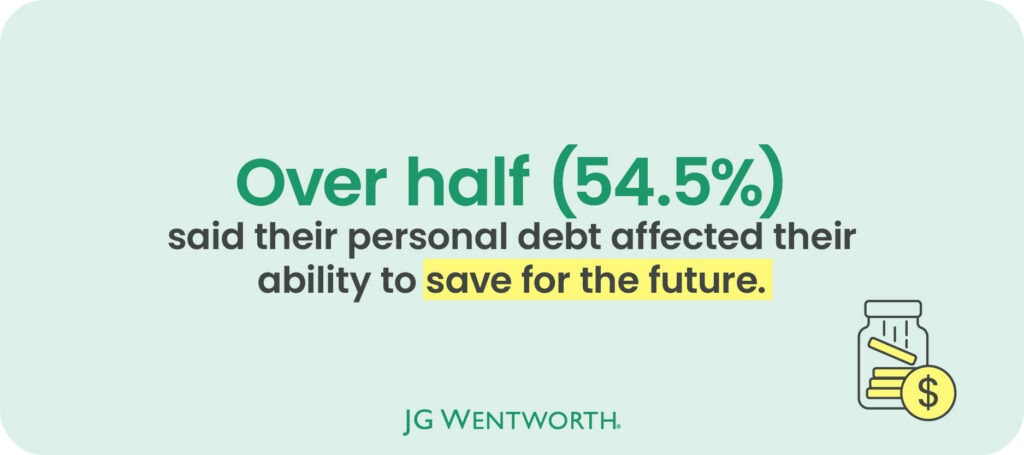

Over half (51%) admitted that their personal debt had significantly affected their ability to cover basic living expenses, such as rent, utilities or groceries. This is echoed by 35.7% who said it had somewhat affected their essential spending. Likewise, a staggering 75.6% admitted to missing or delaying payments because of their personal debt situation. Alongside this, almost two in five (39.9%) said this debt had caused them a significant amount of stress, anxiety, or affected their day-to-day lives. A previous study we conducted in September 2025 found that credit card debt is the most stressful form of debt, and 47% of U.S. adults worried about their debt everyday. Not only that, but half of participants (54.5%) reported that their personal debt had affected their ability to save for the future, including for retirement or unexpected emergencies. Another 38.3% said it had somewhat limited their ability to save, while just 7.3% felt that their savings had not been impacted at all.

In addition, almost half of participants (49.7%) said they had to make significant changes to their lifestyle as a result of taking on debt, such as cutting back on leisure, travel, or hobbies. Even more concerning, 44.7% admitted that their debt had limited their ability to pursue opportunities, including furthering their education, advancing in their careers, or relocating for a job.

Over two-fifths admit their debt has affected their personal relationships

In our recent study, we found that 75.1% of those who have borrowed or lent money from friends or family are no longer as close as they used to be. The impact of debt on personal connections goes beyond these situations, with over three quarters (79.5%) reporting that their personal relationships had been affected by their debt to some level. In contrast, just one in five (20.5%) said it hadn’t had any impact at all.

Methodology

The survey was conducted between January and February 2026 and asked 1,011 adults in the U.S. from a range of backgrounds questions surrounding their personal debt, including what caused them to take this debt on and how they have managed it alongside other financial responsibilities. For some questions, respondents were able to select multiple answers, therefore the results do not all add up to 100%. The demographics of the survey respondents were: Gender:- Male – 55.8%

- Female – 42.4%

- Prefer not to say – 1.3%

- Non-binary – 0.3%

- Not listed – 0.2%

- 18-28 – 11.4%

- 29-44 – 69.9%

- 45-60 – 16.3%

- 61-79 – 2.3%

- 80+ – 0.1%

Sources

[1] Federal Reserve Bank of New York, ‘HOUSEHOLD DEBT AND CREDIT REPORT (Q4 2025)’, 2025

[2] Experian, ‘Average American Debt by Age, US State, Credit Score and Type in 2025’, 2025

[3] GoBankingRates, ‘5 Common Emergency Expenses — And How Much They Cost on Average’, 2024

[4] WalletHub, ‘Medical Debt Statistics’, 2025

[5] U.S. Bureau of Labor Statistics, ‘Consumer Price Index Summary’, 2026

[6] U.S. Bureau of Labor Statistics, ‘Civilian unemployment rate’, 2026

[7] Pew Research Center, ‘8 facts about divorce in the United States’, 2025

[8] Motley Fool Money, ‘The Average Cost of a Divorce’, 2025

[9] United States Courts, ‘Bankruptcy Filings Rise 14.2 Percent’, 2025

[10] Bankrate, ‘Survey: Nearly 3 in 4 Americans have a financial regret’, 2025

About the author