On this page

What's next

Start Your Free Debt Relief Consultation

How much sleep are Americans losing due to debt stress?

by

JG Wentworth

•

April 7, 2026

•

13 min

Our new survey has discovered that financial stress is costing Americans their sleep, with most respondents (94.6%) losing at least some rest due to money worries. This can mean losing hours of sleep on affected nights and multiple nights throughout the week.

To better understand how debt and financial stress affect sleep, we surveyed 1,377 U.S. adults about how their finances impact sleep quality, including how many hours they lose and how often disruption occurs every week.

Given the importance of sleep as a foundation of overall health, supporting physical wellbeing, mental function, and even your social life, [1] this raises important questions: how much sleep is actually being lost, and at what point does debt begin to impact how often people lose sleep each week?

Key findings

- Overall, most respondents (94.6%) experience some level of sleep disruption from financial stress.

- Over one in four (28%) respondents report losing two to three hours of sleep on nights when financial stress affects them.

- One in four respondents (25%) has their sleep disrupted three to four nights per week due to financial worries.

- More than a third (34.5%) of those whose sleep is disrupted every night earn between $10,000 and $49,999 per year, highlighting the impact on different income groups.

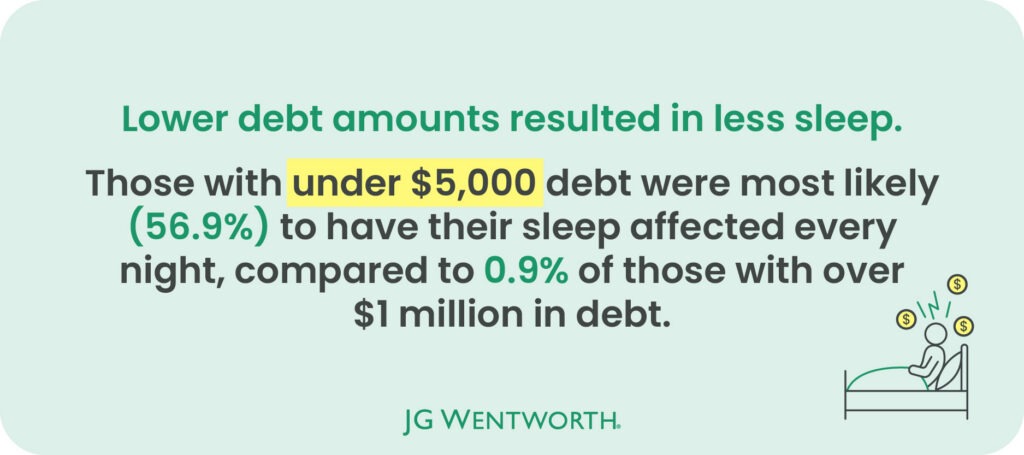

- Those with smaller debts under $5,000 were most likely (56.9%) to have their sleep affected every night, compared to just 9% of those with over $1 million in debt.

How common is debt across America?

In the survey, three in four respondents (75%) said they hold some form of debt, underscoring its prevalence among Americans, and only 25% report being debt-free.

To understand the scale of their debt burden, we asked them how many outstanding debts they have and their total debt balance. With recent data showing that U.S. consumer debt has reached $18.8 trillion, the findings show how widespread and significant debt has become. [2] The most common responses indicated that many people are managing multiple debts at once: two (24%) and three (22%). The largest share of total debt balances fell between $5,000 and $25,000, including 17% owing $10,000-$25,000 and 15% owing $5,000-$10,000.

Financial pressure is also one of the most common sources of stress in the U.S., with two-thirds (66%) of Americans acknowledging money as a significant stressor. [3] Our previous research delving into how debt affects stress levels revealed that over half of the respondents (53.4%) believed debt to be a normal part of life in today’s society.

Financial stress is costing Americans their sleep

Most Americans (77%) lose sleep over money worries at least some of the time, according to the Sleep Foundation, showing how common financial worries are and how deeply they can affect people’s everyday lives. [4]

However, nearly all respondents (94.6%) reported that financial worries disrupt their sleep at least once per week, highlighting how widespread the impact is.

Overall, the survey results found that financial stress can significantly affect sleep quality, with over half (51%) reporting losing up to three hours of sleep a night and nearly two-thirds (60%) having up to four days of sleep being disrupted per week.

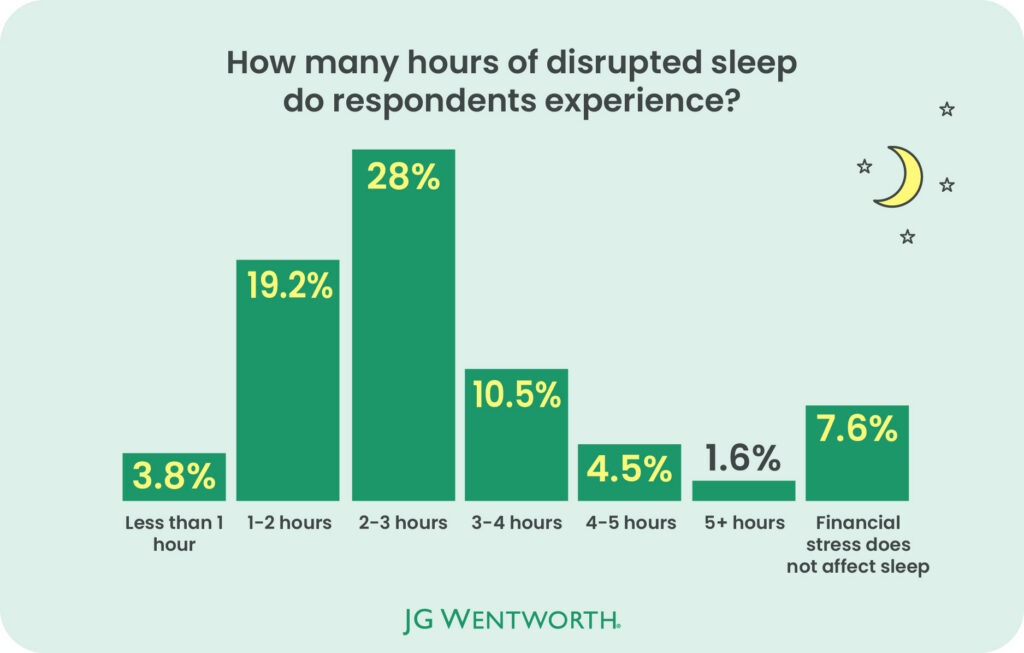

Respondents lose an average of 2.2 hours of sleep per night due to debt worries

The research found that respondents lose an average of 2.2 hours of sleep on nights when their sleep is disrupted due to debt worries.

The most common loss reported was two to three hours, affecting over a quarter (28%) of those surveyed. A further 19% said they typically lose one to two hours, while 11% report losing as much as three to four hours of sleep.

According to the National Sleep Foundation, seven to nine hours of sleep is recommended for adults (ages 18-64), meaning that three hours represents between 33% and 43% of sleep, a significant portion to lose. [5]

On average, respondents experience disrupted sleep on 2.7 nights per week

The survey results revealed that respondents’ sleep is disturbed for almost half the week (2.7 nights per week) on average due to financial stresses. This indicates a huge issue and how stressful debt can be for individuals.

Money stress affects sleep for almost all those surveyed (94.6%), with the most common response being one to two nights per week (35%) and one in four respondents (25%) saying their sleep is disrupted three to four nights per week. Some respondents reported more frequent disruption, with 3.4% saying financial worries affect their sleep five to six nights per week and 6.3% reporting disrupted sleep every single night.

This demonstrates how significantly financial health can impact everyday life. Interrupted sleep can affect thinking, memory, and decision-making, and has also been linked to health issues such as depression, highlighting the potential impact financial stress may have on a person’s overall well-being. [6]

Over a third (34.5%) of those earning between $10,000 and $49,999 lose sleep every night

More than a third (34.5%) of respondents whose sleep is disrupted every night by financial worries earn between $10,000 and $49,999 per year. This number is disturbing, especially considering the median personal income in the U.S. was $40,480 in 2024, [7] giving us insight into how prevalent experiencing broken sleep and potentially other knock-on effects from finances could be.

It came as no surprise that over half of those (51.7%) without any personal income were worried about their finances, so much so that they lost sleep every night. Though the same results contradict that, more than a third of those with no income (33.5%) said that they never lose sleep over finances. Those two polar-opposite responses could signify very different financial circumstances, with unemployment rates being linked with young adults living in a parent’s home, which could potentially be why there’s a significant number of those without income losing no sleep. [8] The results also showed that some of those with no income have better sleep than those who earned over $150,000, with 33.5% compared to 2.9% saying that they never have disrupted sleep due to financial worries.

How many nights of sleep are disrupted each week by income group

| Income group | 0 nights (%) | 1–2 nights (%) | 3–4 nights (%) | 5–6 nights (%) | Every night (%) |

|---|---|---|---|---|---|

| $0 | 33.50% | 13.30% | 12.80% | 10.70% | 51.70% |

| $1 – $9,999 | 7.10% | 20.80% | 13.00% | 9.20% | 2.60% |

| $10,000 – $24,999 | 17.70% | 20.80% | 25.50% | 29.00% | 17.20% |

| $25,000 – $49,999 | 12.90% | 14.10% | 21.30% | 33.60% | 17.20% |

| $50,000 – $74,999 | 7.10% | 18.40% | 17.90% | 12.20% | 5.20% |

| $75,000 – $99,999 | 8.80% | 7.90% | 5.90% | 3.80% | — |

| $100,000 – $149,999 | 5.90% | 3.80% | 2.90% | 1.50% | 1.70% |

| $150,000 and greater | 2.90% | 0.80% | 0.50% | — | 0.90% |

Smaller debts are most likely to keep Americans awake

You’d be forgiven for assuming that more debt equals more worries, but the survey results showed something different. The pattern was inverted, showing that debt numbers were not necessarily an indicator of how much sleep would be lost.

When we asked respondents how often their sleep was disrupted each week, those in debt of under $5,000 were most likely (56.9%) to have their sleep affected every night, whereas those with over a million dollars in debt were among the least likely (0.9%) alongside $750,000-$1 million (0.9%), and $100,000-$250,000. Proving that smaller debts can be just as, if not more stressful than significantly larger debt sums.

Sleep disruption by type of debt

Sleep disruption varied depending on the type of debt that respondents had. We asked them to score their sleep out of five, with five being the most disrupted and one being the least disrupted.

The types of debts included mortgages, overdrafts/bank fees, personal loans, and other debts, including debt to family and friends, something known as shadow debt, with over half of respondents (51.6%) from a previous survey saying they have had this type of debt at least once. Here’s a ranking of the most disruptive debt for sleep from most to least disruptive.

Sleep disruption rating by type of debt

| Type of debt | Average sleep disruption rating (out of five) |

|---|---|

| Mortgage | 3.24 |

| Overdraft/bank fees | 3.16 |

| Personal loans | 3.11 |

| Medical debt | 3.06 |

| Auto loans | 2.99 |

| Student loans | 2.84 |

| Debt to family/friends | 2.83 |

| Payday loans | 2.8 |

| Credit card debt | 2.58 |

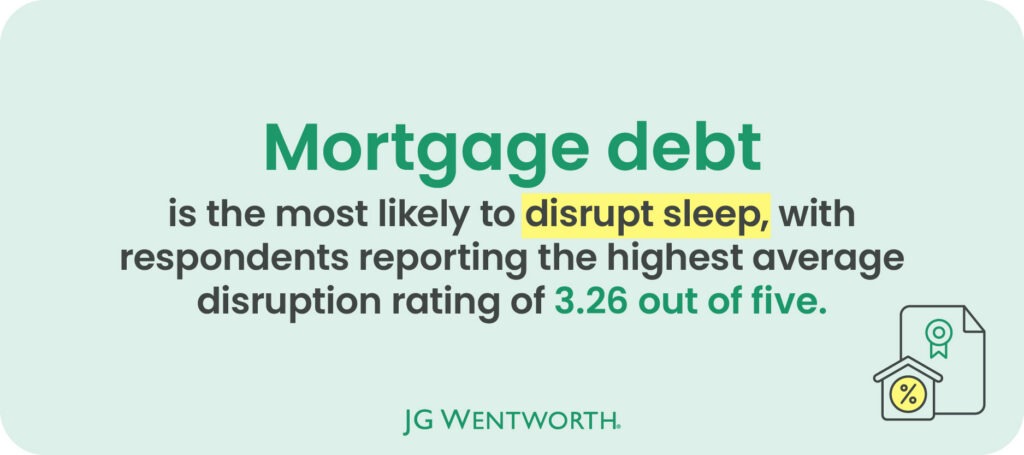

Mortgages had the highest disruption rating (3.24 out of five)

Mortgages were most likely to disrupt sleep, with the highest average rating of disruption, with a score of 3.24. This may reflect wider market conditions, with mortgage rates more than doubling in recent years, rising from around 3% in 2021 to over 7% in 2023, remaining above 6% through 2024, and continuing at elevated levels into 2026, increasing monthly repayments for many homeowners. [9]

Overall, only 8.9% of respondents picked a score of one (the least disrupted sleep) in regards to their mortgage, whereas 14.2% picked five, and most respondents picked either three (31.4%) or four (29.5%).

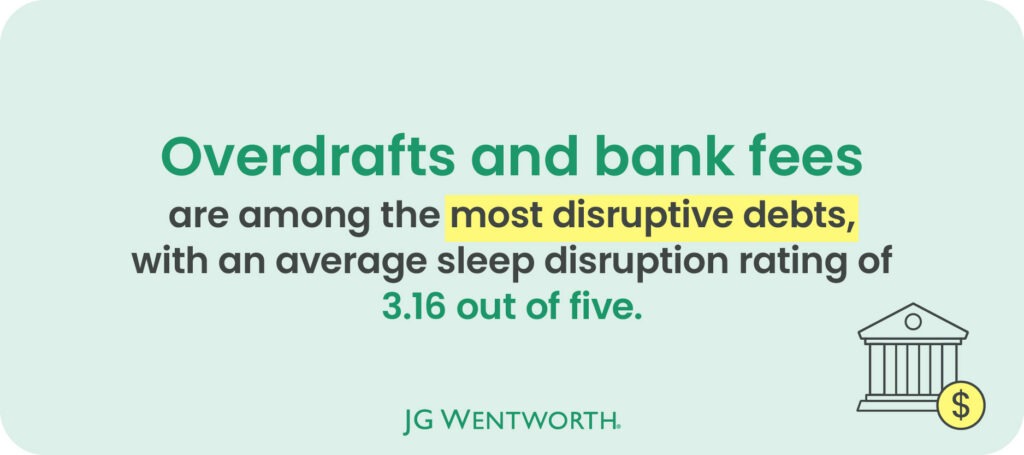

Overdraft and bank fees were also the cause of sleepless nights, with a 3.16 disruption rating

Overdrafts and bank fees were a significant source of sleep disruption, with an average rating of 3.16 out of five.

Responses were weighted toward the higher end of the scale, with over a quarter (26.4%) rating their sleep disruption as four and 13.8% selecting the maximum score of five regarding their overdraft and bank fees. While fewer respondents (8.6%) reported no impact at all, the largest share (30%) sat in the middle, indicating that this type of debt consistently affects sleep for many.

Personal loans were significantly disruptive (3.11 rating)

Personal loans were a major contributor to sleep disruption, with an average rating of 3.11 out of five.

Responses leaned toward moderate to high disruption, with 32% selecting three and a further 25% choosing four, while 13.4% reported the highest level of impact. Only 11.4% said their sleep was not affected at all, showing that personal loan debt commonly interferes with sleep.

Over a quarter (27.2%) of those in debt experience mood swings

Over a quarter (27.2%) of respondents in debt report experiencing mood swings from the stress of their finances. In addition to sleep disruption, there were lots of other ways in which debt and finances affected respondents’ everyday lives.

Mood swings (27.2%) were the most common answer, followed by anxiety/panic (23.6%), and appetite changes/eating habits (16.5%). Other symptoms such as headaches and fatigue were reported by 14.6%, relationships with friends and family were affected for 11% of respondents, and 6.2% said their work productivity was impacted. Only 8.6% of respondents said they were not affected in any other way (other than sleep).

This shows how our finances can seep into our day-to-day lives, even spilling into emotional well-being, physical health, relationships, and day-to-day functioning.

How financial stress affects respondents

| Symptom | Percentage of respondents (%) |

|---|---|

| Mood swings/irritability | 27.20% |

| Anxiety/panic | 23.60% |

| Appetite changes/eating habits | 16.50% |

| Physical health (e.g., headaches, fatigue) | 14.60% |

| Relationships with family/friends | 11.00% |

| It does not affect me any other way | 8.60% |

| Work performance/productivity | 6.20 |

*Data note: Respondents were able to pick more than one answer

Monthly bills, debts, and the cost of living are the leading causes of financial stress

When considering that over half (56%) of Americans have paid a bill late at least once, it’s no surprise that many find keeping on top of monthly bills stressful. [10] Paying monthly bills such as rent, utilities, and phone bills (16.1%) was picked as the biggest source of financial stress by respondents, followed by debt (13%), and rise of living costs (12.2%).

With debt ranking as the second biggest source of financial worry, its impact is amplified by how widespread it is, with three-quarters (75%) of respondents holding at least one form of debt.

This shows that financial stress linked to debt is not isolated, but affects a large share of respondents, reinforcing its role as a key driver of disrupted sleep and overall well-being.

How financial stress affects respondents

| Financial stress | Percentage of respondents (%) |

|---|---|

| Paying monthly bills (rent, utilities, phone, etc.) | 16.10% |

| High total debt amount | 13.00% |

| Rise in the cost of living | 12.20% |

| Unexpected expenses (medical bills, car repairs, etc.) | 9.70% |

| Saving for future goals (retirement, education, major purchases) | 6.80% |

| Lack of financial knowledge/budgeting challenges | 6.00% |

| Supporting family | 4.70% |

| Job insecurity or unstable employment | 1.80% |

| Unemployment | 1.60% |

| Business or self-employment financial concerns | 1.20% |

| Credit score/fear of loan denial | 0.70% |

| Insurance payments (health, auto, home) | 0.70% |

| Managing taxes | 0.70% |

*Data note: Respondents were able to pick more than one answer

How people are trying to manage financial stress

As financial stress takes its toll on both mental and physical health for some of the respondents, leading to anxiety, sleep disruption, and mood swings, many people have also started taking measures to combat these negative effects on their daily lives.

Guidance shows that money worries can damage self-esteem and lead to depression, as well as changes in weight. Some useful steps to manage these challenges include talking to family and friends, making a plan, creating a monthly budget, and managing stress through exercise, healthy eating, and sufficient sleep. [11]

Respondents had evidently considered some of the same logic by choosing a number of useful ways to manage their financial stress. With more than one in five people (21.8%) saying that they are involved in exercise as a way to help them deal with their money stresses, while others meditated (21.4%), tried to improve their sleep with routines (18.7%) or spoke to their family, friends or therapists (14.7%), and created monthly budgets and plans (10.3%).

Fortunately, only 4.4% said that they hadn’t taken any steps towards managing their financial stress.

Steps taken by respondents to manage financial stress

| Steps taken | Percentage of respondents (%) |

|---|---|

| Exercise/physical activity | 21.80% |

| Meditation/mindfulness exercises | 21.40% |

| Sleep hygiene routines | 18.70% |

| Talking with family, friends, or a therapist | 14.70% |

| Budgeting / financial planning | 10.30% |

| Professional help | 7.60% |

| No action taken | 4.40% |

*Data note: Respondents were able to pick more than one answer

Methodology

The survey was conducted on behalf of JG Wentworth in March 2026 and asked 1,377 U.S. adults about how their finances impact their sleep quality, including how many hours they lose and how often disruption occurs every week. The survey also delved into what respondents considered to be the most stressful forms of debt and steps taken to overcome the negative impact.

Demographics of the survey:

Age:

- 29-44 – 59.8%

- 18-28 – 19.4%

- 45-60 – 18.4%

- 61-79 – 2.1%

- 80+ – 0.3%

Gender:

- Female – 69.9%

- Male – 26.7%

- Non-binary – 1.7%

- Not listed – 1.0%

- Prefer not to say – 0.7%

Personal Income Level:

- $0 – 29.6%

- $1 – $9,999 – 10.9%

- $10,000 – $24,999 – 16.8%

- $25,000 – $49,999 – 16.7%

- $50,000 – $74,999 – 11.4%

- $75,000 – $99,999 – 9.2%

- $100,000 – $149,999 – 3.6%

- $150,00 and greater – 1.2%

- Prefer not to say – 0.7%

Sources

[1] PubMed Central ‘Financial Stress and Sleep Quality’

[2] Federal Reserve Bank of New York, ‘Household Debt and Credit Report’

[3] American Psychological Association ‘Stress in America 2025’

[4] Sleep Foundation ‘77% Lose Sleep to Financial Worries’

[5] National Sleep Foundation ‘How Many Hours of Sleep Do You Really Need?’

[6] Sleep Foundation ‘Interrupted Sleep’

[7] Federal Reserve Bank of St. Louis ‘Median Personal Income in the United States’

[8] Pew Research Center ‘The Shares of Young Adults Living With Parents Vary Widely Across the U.S.’

[9] Freddie Mac ‘Primary Mortgage Market Survey’

[10] The Motley Fool ‘Late Bills Statistics’

[11] HelpGuide ‘Coping with Financial Stress’

About the author