On this page

What's next

Earn a high-yield savings rate with JG Wentworth Debt Relief

America On The Brink of Bankruptcy

by

JG Wentworth

•

March 17, 2026

•

12 min

Between September 2024 and September 2025, non-business bankruptcy filings rose by 10.8%, [1] reflecting the growing financial pressures faced by households. Many factors can push individuals toward bankruptcy, from the rising cost of living to mounting personal debt.

To better understand how bankruptcy affects people across the U.S., we surveyed 1,421 adults across America about their experiences and financial struggles. The survey explores key topics such as what contributes to bankruptcy, the emotional stress of filing, and how individuals rebuild their finances afterward.

Key findings:

- The cost of living crisis is the leading contributor to bankruptcy (43.4%), followed by increased tariffs (41.7%) and medical expenses (3.7%).

- Nearly nine in ten (89.3%) people who have filed for bankruptcy were able to rebuild financially, but it took as long as five years.

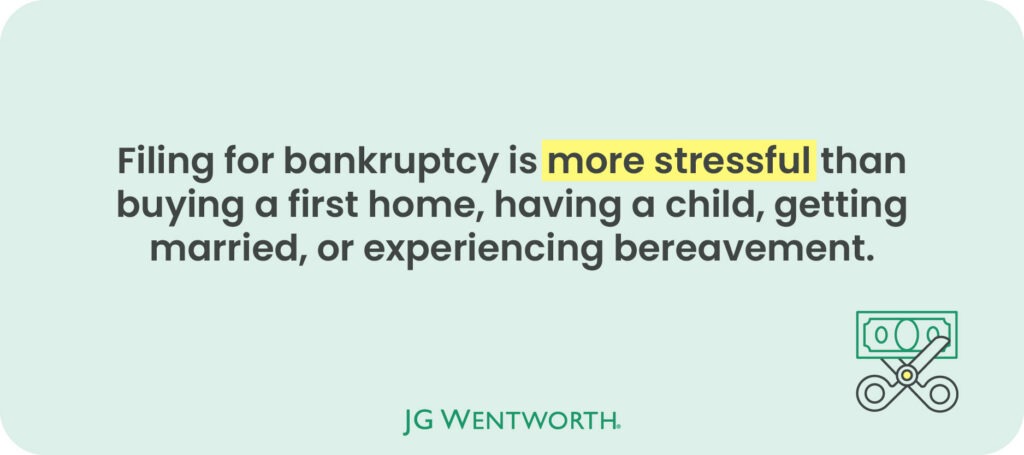

- Participants say filing for bankruptcy is more stressful than having a baby (35.5%) or buying a first home (36.6%).

- 8% said they are still feeling the effects of their bankruptcy today, regardless of how long ago they filed or whether they have financially recovered.

- Almost three quarters (73.7%) reported that bankruptcy still affects their ability to get loans or credit, and 73.3% said their credit score continues to be affected.

- On average, it would take $6,356.55 of additional debt to push Americans to the brink of bankruptcy.

- When asked how many months of expenses they could cover if their income suddenly stopped, 40.8% of participants said they could manage for just three months.

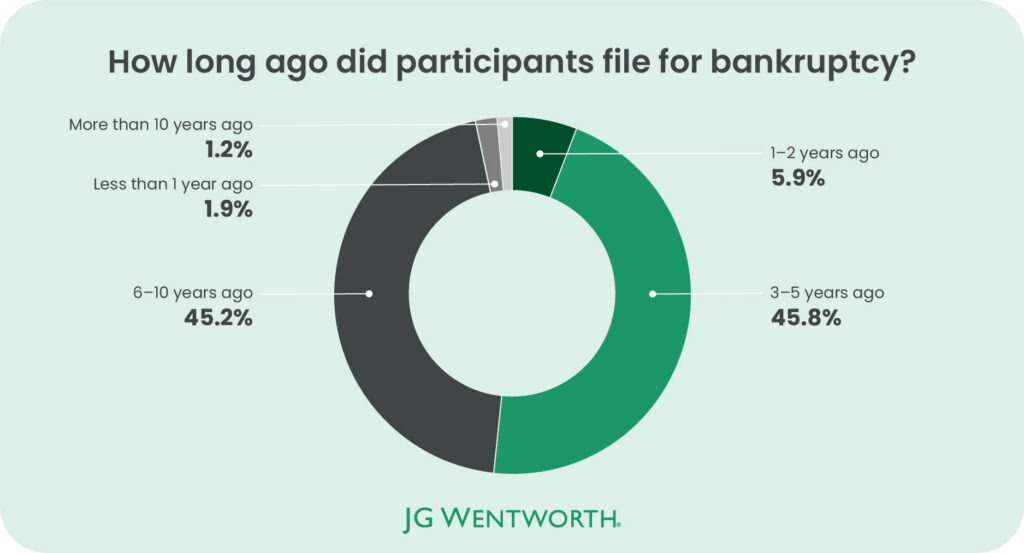

How common is bankruptcy in America?

Among respondents who reported filing for bankruptcy, the timing was split almost evenly. About 45.8% said they filed 3-5 years ago, while 45.2% reported filing 6-10 years ago.

Summary

- Non-business bankruptcy filings rose 10.8% between September 2024 and September 2025, reflecting intensifying financial pressure on U.S. households.

- The cost of living crisis is the leading self-reported contributor to bankruptcy at 43.4%, followed by increased tariffs at 41.7% and medical expenses at 3.7%.

- On average, just $6,356 of additional debt beyond existing obligations would push a typical American respondent to the brink of bankruptcy.

The cost of living crisis is the leading contributor to bankruptcy (43.4%)

When respondents were asked what most contributed to their bankruptcy, the cost of living crisis emerged as the top factor, cited by 43.4% of participants. Increased tariffs followed closely behind, mentioned by 41.7%. Tariffs are taxes on imported goods, and businesses may pass these added costs on to consumers, which can raise the prices of everyday items and place additional strain on household finances. [2] Although conversations around tariffs have become more prominent in the last year or two, discussions about raising them date back to 2018 when the U.S. noted plans to impose a 25% tariff on cars imported from the European Union. [3]

The main contributors to bankruptcy

| Rank | What was the main contributor that led to bankruptcy? | Percentage of participants |

|---|---|---|

| 1 | Cost of living crisis | 43.40% |

| 2 | Increased tariffs | 41.70% |

| 3 | Medical expenses | 3.70% |

| 4 | Credit card or personal loan debt | 3.20% |

| 5 | Job loss or reduced income | 2.60% |

| 6 | Business failure | 1.60% |

| 7 | Student loans | 1.10% |

| 8 | Overspending / lifestyle choices | 0.70% |

| 9 | Divorce or family breakdown | 0.50% |

| 10T | Interest rate increases | 0.30% |

| 10T | Mortgage increases | 0.30% |

| 10T | Poor financial planning | 0.30% |

| 13T | Death of a loved one (i.e. funeral costs) | 0.20% |

| 13T | Other unexpected expenses | 0.20% |

On the other hand, factors such as mortgage and interest rate increases (0.3% each), poor financial planning (0.3%), the death of a loved one (0.2%), and unexpected expenses (0.2%) were far less commonly cited. Despite this, a report from Debt.com found that more than one in three people (37%) take on debt after the death of a loved one, often to cover funeral or medical expenses. [4]

Nearly nine in ten (89.3%) were able to rebuild financially, but it took as long as five years

The survey also asked participants whether they had successfully rebuilt their finances following filing for bankruptcy. Nearly nine in ten (89.3%) reported that they had, typically taking 3-5 years to recover. In contrast, just 1% said they were still struggling financially.

Among those who hadn’t fully rebuilt, the leading reason, highlighted by 88.4%, was high living costs and rising expenses. This was followed closely by ongoing low income or unemployment (85.8%) and continued medical expenses or health issues (82.5%).

Reasons why participants weren’t able to rebuild financially after bankruptcy

| Rank | Reasons for not rebuilding financially | Percentage of respondents |

|---|---|---|

| 1 | Ongoing low income or unemployment | 88.40% |

| 2 | High living costs / cost of living increase | 85.80% |

| 3 | Continued medical expenses or health issues | 82.50% |

| 4 | Outstanding debts that weren’t discharged | 74.20% |

| 5 | Lack of financial knowledge or guidance | 4.20% |

| 6 | Dependents or family financial obligations | 3.50% |

| 7 | Poor budgeting or financial management | 2.90% |

| 8 | Impact of previous bankruptcy on credit and borrowing | 1.60% |

| 9 | Unexpected life events (divorce, business failure, etc.) | 0.90% |

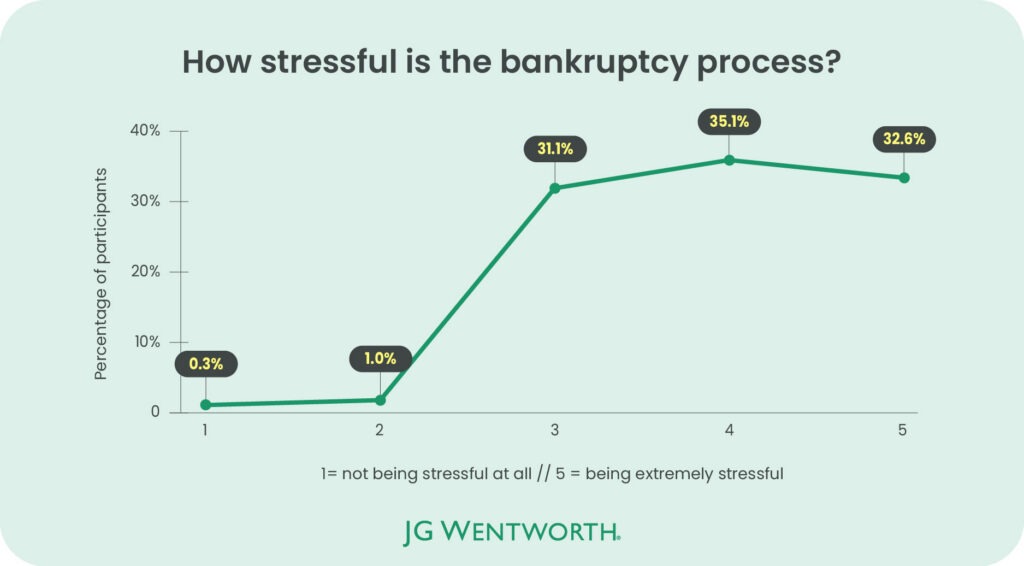

How much stress does bankruptcy cause?

More than one in three respondents (35.1%) rated the stress of bankruptcy as high as four out of five, with one being not stressful at all and five being extremely stressful. An additional 32.6% gave it the maximum rating of five out of five.

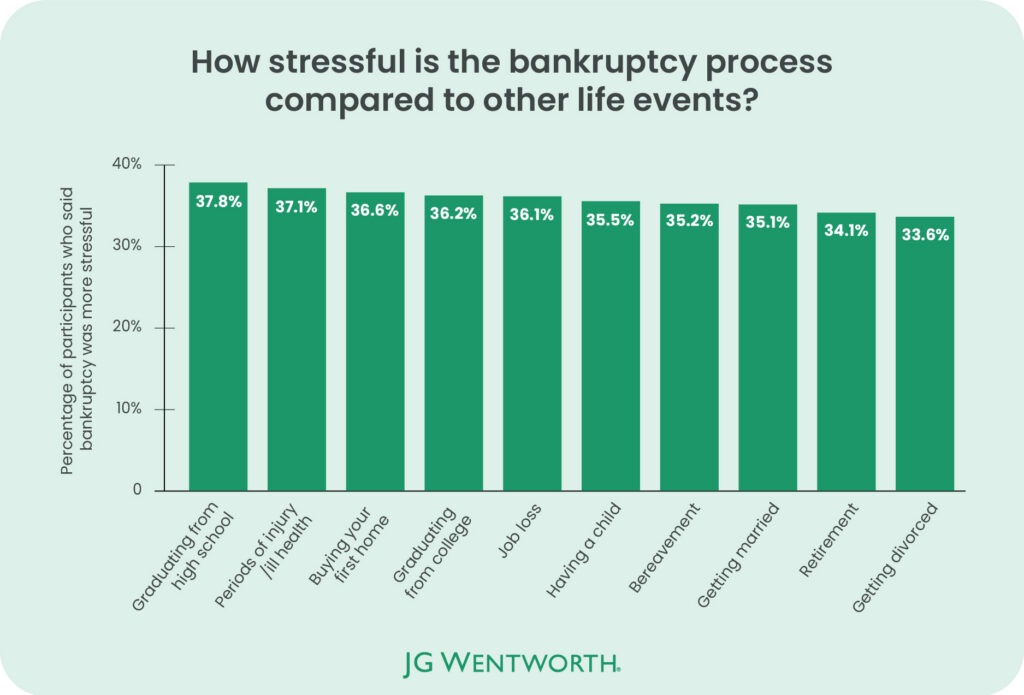

Filing for bankruptcy is more stressful than having a baby or buying a first home

Among those who had previously filed for bankruptcy, the survey asked them to compare the stress of the process with other major life events. Many said bankruptcy was more stressful than several key events, including buying their first home (36.6%) said filing for bankruptcy was more stressful) and even having a child (35.5%).

The only life event considered equally stressful was getting a divorce, with 33.6% of respondents saying it was less stressful and 33.6% saying it was more stressful than bankruptcy.

How does bankruptcy affect everyday life?

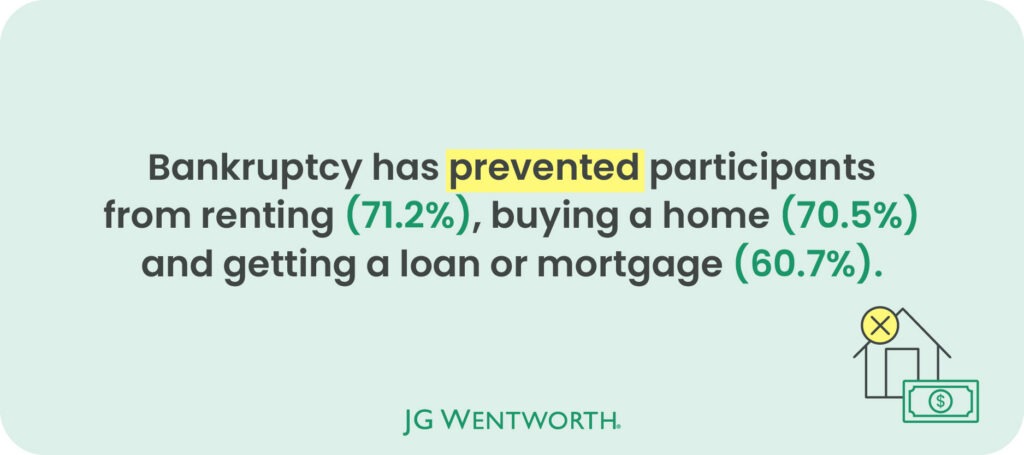

Bankruptcy can have profound and enduring consequences for everyday life. To learn more about this, the survey explored the real-life impact of bankruptcy on adults across the U.S. For nearly three quarters of respondents (71.2%), filing for bankruptcy prevented them from renting a home or apartment, while 70.5% were prevented from buying a house or property. Almost two thirds (60.7%) also said bankruptcy had stopped them from obtaining a loan or mortgage.

What has bankruptcy prevented participants from doing?

| Rank | Preventions | Percentage of participants |

|---|---|---|

| 1 | Renting a home or apartment | 71.20% |

| 2 | Buying a house or property | 70.50% |

| 3 | Getting a loan or mortgage | 60.70% |

| 4 | Using credit cards or taking out new credit | 43.50% |

| 5 | Starting or running a business | 27.30% |

| 6 | Making large purchases (car, appliances, etc.) | 3.70% |

| 7 | Traveling or taking holidays | 3.20% |

| 8 | Pursuing higher education or student loans | 3.10% |

| 9 | Saving for the future or retirement | 2.60% |

*Participants could select multiple options.

Almost all participants who have filed for bankruptcy are still feeling the effects today (97.8%)

In addition to this, an overwhelming 97.8% of respondents said they are still feeling the effects of their bankruptcy today, regardless of how long ago they filed or whether they have financially recovered. Almost three quarters (73.7%) reported that bankruptcy has had a lasting impact on their ability to obtain loans or credit, and 73.3% said their credit score continues to be affected.

Lasting effects of bankruptcy

| Rank | Effects of bankruptcy | Percentage of participants |

|---|---|---|

| 1 | Difficulty getting loans or credit | 73.70% |

| 2 | Credit score is still affected | 73.30% |

| 3 | It impacts participants ability to rent a home | 60.70% |

| 4 | It affects participants ability to start a business | 43.10% |

| 5 | It affects participants financial confidence or decision-making | 29.20% |

*Participants could select multiple options.

In contrast, under a third of respondents (29.2%) said bankruptcy had impacted their confidence in making financial decisions.

Nearly a third (29%) of bankruptcy filers say they’re struggling financially

Among participants who have filed for bankruptcy, nearly a third (29%) said their current financial situation is very difficult. Another 27.7% described it as somewhat difficult, and 29.9% said they are just managing. Only 5.6% said they are currently managing comfortably.

By comparison, 45.5% of participants who have never filed for bankruptcy reported managing comfortably, while just 6.1% said they were struggling significantly.

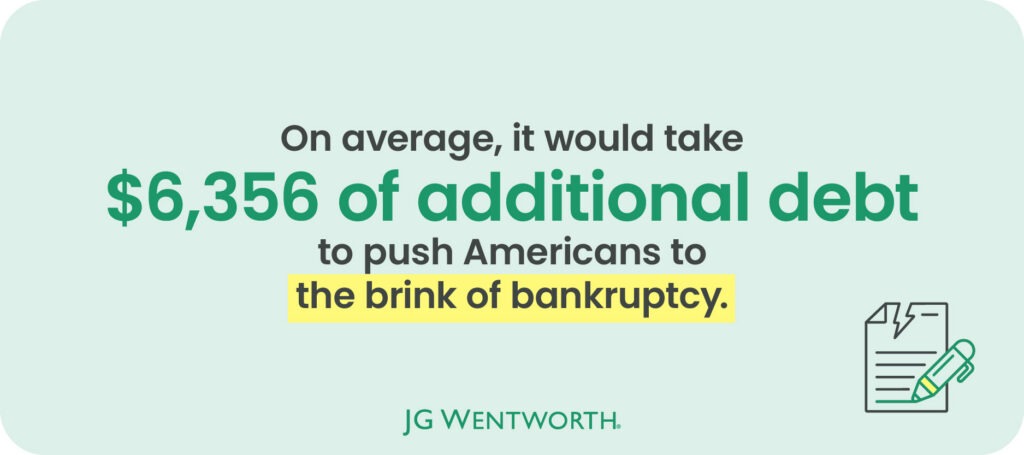

How close are Americans to bankruptcy?

The survey asked participants how much additional debt beyond their mortgage would push them into bankruptcy. On average, participants said this totalled just $6,356.

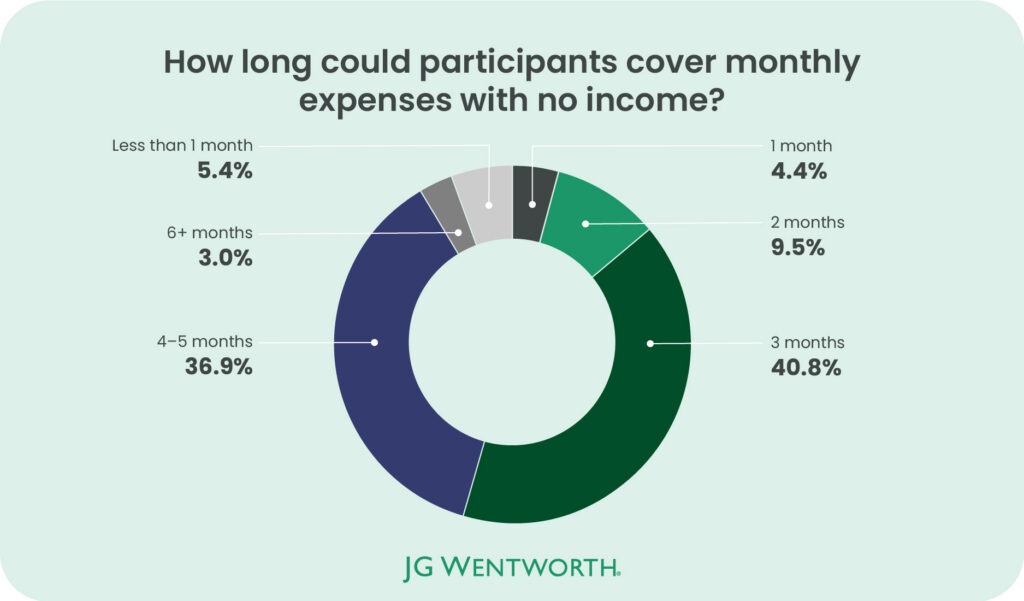

Participants were also asked how many months of expenses they could cover if their income suddenly stopped. The most common response was three months, cited by 40.8% of all respondents.

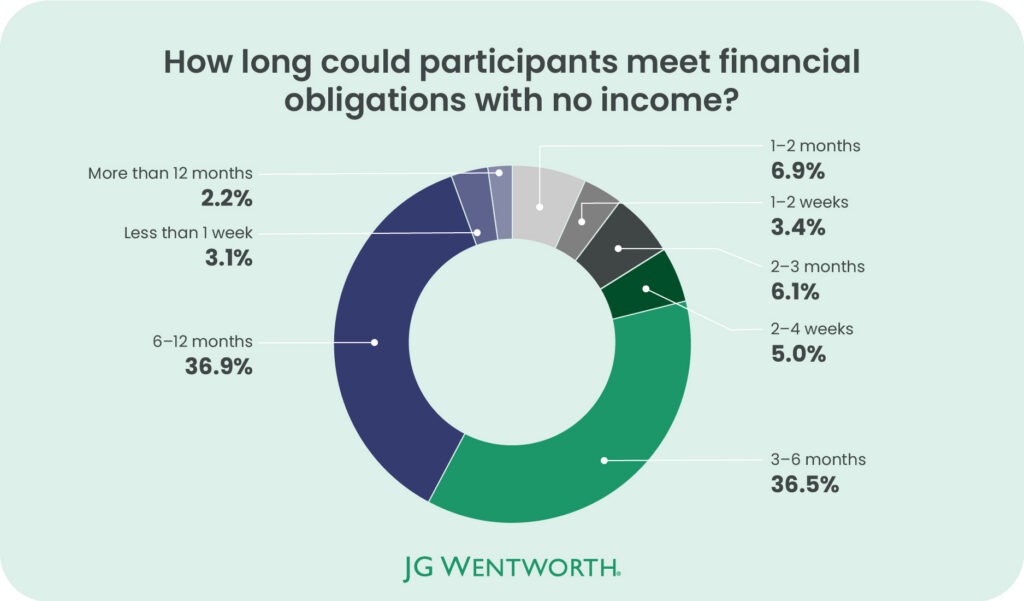

In addition, participants were asked how long they could continue meeting their financial obligations if their income stopped today. The most common response was 6-12 months (36.9%), followed closely by 3-6 months (36.5%).

How would Americans cope with financial trouble?

To better understand how individuals might respond to severe financial strain, the survey asked participants which strategies they would turn to if their debt became unmanageable. The most common responses were borrowing from family or friends (79.4%), using credit cards to cover expenses (78.2%), and taking out personal loans (71.4%).Common coping strategies

| Rank | Coping strategy | Percentage of participants |

|---|---|---|

| 1 | Borrowing from family/friends | 79.40% |

| 2 | Using credit cards to cover expenses | 78.20% |

| 3 | Taking out personal loans | 71.40% |

| 4 | Selling assets (car, home, valuables) | 61.60% |

| 5 | Declaring bankruptcy | 40.70% |

| 6 | Cutting essential or discretionary expenses | 11.80% |

*Participants could select multiple options.

Yet fewer participants said they would rely on cutting essential or discretionary expenses (11.8%) or declaring bankruptcy (40.7%) as coping strategies for financial hardship.

When asked what they would do first in such a situation, the results changed significantly. The most popular initial strategy was cutting essential or discretionary expenses (41.5%), followed by declaring bankruptcy (34.6%).

Top coping strategies when facing financial difficulties

| Rank | Top coping strategy | Percentage of participants |

|---|---|---|

| 1 | Cutting essential or discretionary expenses | 41.50% |

| 2 | Declaring bankruptcy | 34.60% |

| 3 | Selling assets (car, home, valuables) | 6.30% |

| 4 | Using credit cards to cover expenses | 5.80% |

| 5 | Taking out personal loans | 5.50% |

| 6 | Borrowing from family/friends | 5.30% |

Borrowing from friends or family (5.3%) and taking out personal loans (5.5%) were among the least common coping strategies. However, a previous study found that 51.6% of respondents have borrowed money from friends or family at least once, while 53% said they have lent money to friends or family, showing that for many, relying on loved ones might be the only option for financial support.

Nearly nine in ten (86.9%) of participants have had to skip essential payments due to financial strain

A staggering 86.9% of respondents reported having to skip essential payments such as rent, utilities, or medical bills because of financial pressure. The most commonly skipped or reduced payments were rent (60.4%), mortgage (59.9%), and gas (48.9%).

What essential payments have participants skipped due to financial strain?

| Rank | Skipped payments | Percentage of participants |

|---|---|---|

| 1 | Rent | 60.40% |

| 2 | Mortgage | 59.90% |

| 3 | Gasoline | 48.90% |

| 4 | Medical insurance | 38.20% |

| 5 | Doctors visits | 26.20% |

| 6 | Credit card payments | 7.50% |

| 7 | Groceries | 5.00% |

| 8 | Student loan payments | 4.70% |

| 9 | Auto loan payments | 4.30% |

| 10 | Other personal loan payments | 2.80% |

| 11 | Heating | 2.50% |

| 12 | Public transport fares | 2.30% |

| 13 | Prescription medication | 2.10% |

| 14 | Childcare | 0.90% |

*Participants could select multiple options.

Dining out tops the list of expenses participants would cut

Alongside this, when asked which expenses participants would reduce if they faced financial difficulties, the most common cuts were dining in restaurants (72.2%), ordering takeout (70.3%), and buying coffee (58.6%).

Which expenses would participants cut back on?

| Rank | Cut back expenses | Percentage of participants |

|---|---|---|

| 1 | Dining in restaurants | 72.20% |

| 2 | Ordering takeout | 70.30% |

| 3 | Buying coffees | 58.60% |

| 4 | Streaming services (Netflix, Spotify, etc) | 44.90% |

| 5 | Buying concert tickets | 30.80% |

| 6 | Vacations | 14.60% |

| 7 | Buying clothing | 11.70% |

| 8 | Buying cosmetic and grooming items | 9% |

| 9 | Hobbies and leisure activities | 8.90% |

| 10 | Gym memberships | 8.70% |

| 11 | Taxi cabs | 8.20% |

| 12 | Gifts for other people | 8% |

| 13T | Attending events, i.e. weddings, birthdays | 7.20% |

| 13T | Socializing | 7.20% |

*Participants could select multiple options.

Meanwhile, participants were less likely to cut back on socialising in general (7.2%), attending events such as birthdays or weddings (7.2%), or buying gifts for others (8%) when facing financial difficulties.

86.5% are only somewhat confident in their ability to recover from a sudden financial crisis

Almost nine in ten respondents (86.5%) said they are somewhat confident in their ability to bounce back if faced with an unexpected financial emergency. In comparison, only 9% said they feel very confident, while 4.5% reported little or no confidence.

A third of participants (33.4%) also highlighted that increasing their income or job security was the answer to improve their financial security. This was followed by better financial education or guidance (27.4%) and health insurance or medical coverage (22.3%).

Methodology

The survey was conducted in February 2026 and asked a total of 1,421 adults in the U.S. from a range of backgrounds questions relating to their experience with bankruptcy. The survey delved into topics such as stress related to the bankruptcy process, coping strategies and how bankruptcy would impact their spending habits.

For some questions, respondents were able to select multiple answers, therefore the results do not all add up to 100%.

The demographics of the survey respondents were:

Gender:

- Female – 57.7%

- Male – 41.9%

- Non-binary – 0.1%

- Prefer not to say – 0.3%

Age:

- 18-28 – 21.5%

- 29-44 – 69.7%

- 45-60 – 7.2%

- 61-79 – 1.5%

- 80+ – 0.1%

Sources

[1] United States Courts, ‘Bankruptcy Filings Increase 10.6 Percent’, 2025

[2] CNBC, ‘Tariffs are ‘simply inflationary,’ economist says: Here’s how they fuel higher prices’, 2025

[3] CNBC, ‘Trump: We are going to put a 25% tariff on every car from the European Union’, 2018

[4] Debt.com, ‘Funeral Debt Survey: More Than 1 in 3 Americans Took on Debt After a Loved One’s Death’, 2026

About the author