On this page

What's next

Start Your Free Debt Relief Consultation

The Average Debt Timeline in the U.S.

by

JG Wentworth

•

May 18, 2026

•

13 min

Research shows that Americans carry over $18.57 trillion in total household debt, with the average consumer owing around $105,444, showing how widespread borrowing has become across everyday finances. According to Experian’s Consumer Debt Study, most of this balance is in mortgages, but millions of Americans also carry credit cards, auto loans, and student debt at the same time. [1]

With this in mind, we analyzed how long it typically takes to repay that debt, based on a survey of 1,376 U.S. adults conducted on behalf of JG Wentworth. The research focused on average repayment timelines, how interest extends debt, and which borrowers remain in debt the longest.

The study found that while some debts are cleared within a few years, others can stretch across decades, especially when interest and lower monthly payments are factored in.

Key findings:

- Interest can add significant time to repayment terms, extending mortgage timelines by 6.8 years, from 10.7 years to 17.5 years, and student loans, rising by 1.6 years, from 5.8 years to 7.4 years on average.

- Among mortgage holders, 14.2% pay up to $500 per month, potentially stretching repayment timeline to around 65 years, compared to 25.6% paying $1,001–$1,501 monthly, which could reduce it to about 13 years.

- On average, students spend almost twice as long paying student debt (7.4 years) as they do studying (4 years for a Bachelor’s Degree).

- Gen Z repay debt the fastest, clearing credit card balances in 9 months compared to around 22 months for Baby Boomers, while carrying significantly lower balances ($1,652 vs $6,327).

- Parents clear their credit card debt in less than half the time than those without children, taking 17 months compared to 36 months, while non-parents carry more than double the balance ($7,088 vs $3,117).

How many Americans are in debt?

More than three in four U.S. households (77.4%) carry some form of debt, according to the Federal Reserve’s latest Survey of Consumer Finances, confirming that borrowing is a standard part of household finances rather than an exception. [2]

This includes a range of common liabilities such as mortgages, credit cards, auto loans, and student loans, with housing debt accounting for the largest share. Federal Reserve data shows that many households manage multiple forms of debt at once, reflecting how borrowing is often tied to essential costs like buying a home, financing a vehicle, or covering education. [2]

While these figures highlight how widespread debt is, they do not show how long people remain in it. That is where repayment timelines become critical, as the length of time it takes to pay off debt can vary significantly depending on factors such as monthly payments and interest rates.

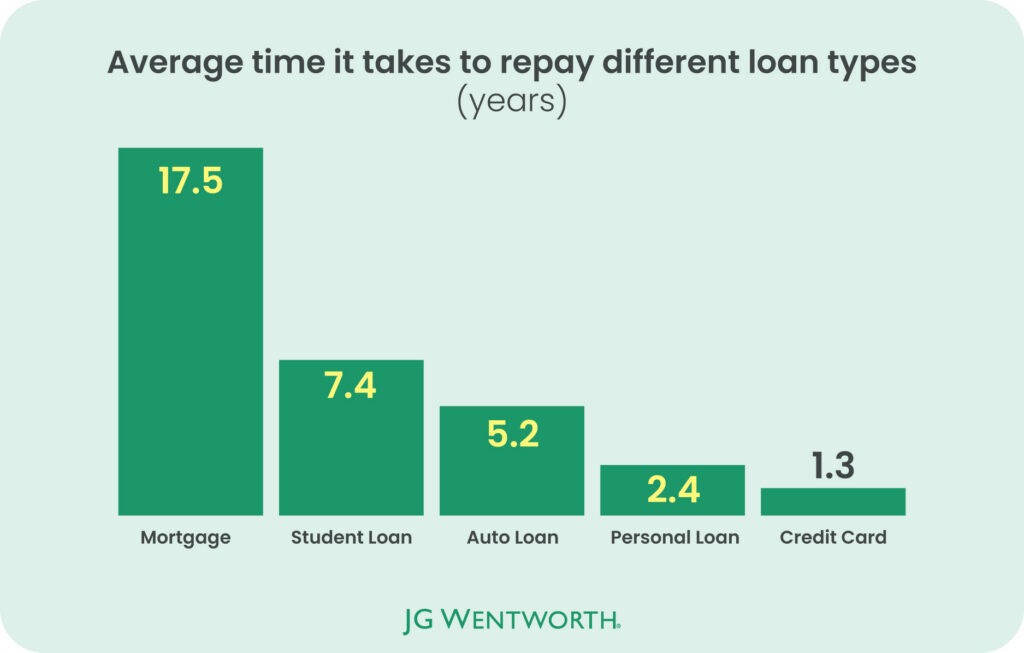

How long it takes to pay off debt by loan type

Repayment timelines vary widely depending on debt type, with some balances cleared in just over a year while others last decades. It’s no surprise that the survey results found that credit cards took the least time to pay on average (1.3 years), while mortgages took the longest at 17.5 years.

| Loan Type | Repayment Time Including Interest (Years) |

|---|---|

| Mortgage | 17.5 |

| Student Loan | 7.4 |

| Auto Loan | 5.2 |

| Personal Loan | 2.4 |

| Credit Card | 1.3 |

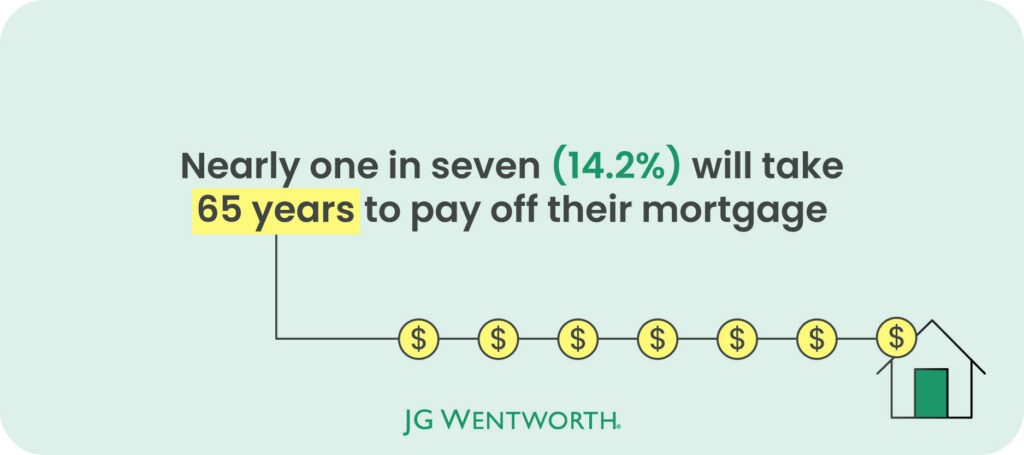

It takes over six decades to pay off a mortgage for one in seven (14.2%)

Among mortgage holders surveyed, around one in seven (14.2%) pay up to $500 per month. At this level, repayment timelines could extend to approximately 65 years, based on the average loan size ($118,200) and a 6.22% interest rate. [3] At the other end, over a quarter (25.6%), paying between $1,001 and $1,501 per month, could reduce this to around 13 years.

On average, mortgages in our survey take 17.5 years to repay, based on an average original loan amount of $118,200 for respondents and the latest 6.22% interest rate as of March 2026. [3] These averages were taken from a range of respondents across different age groups and property types, meaning that loan sizes and repayment timelines vary depending on when and what was purchased.

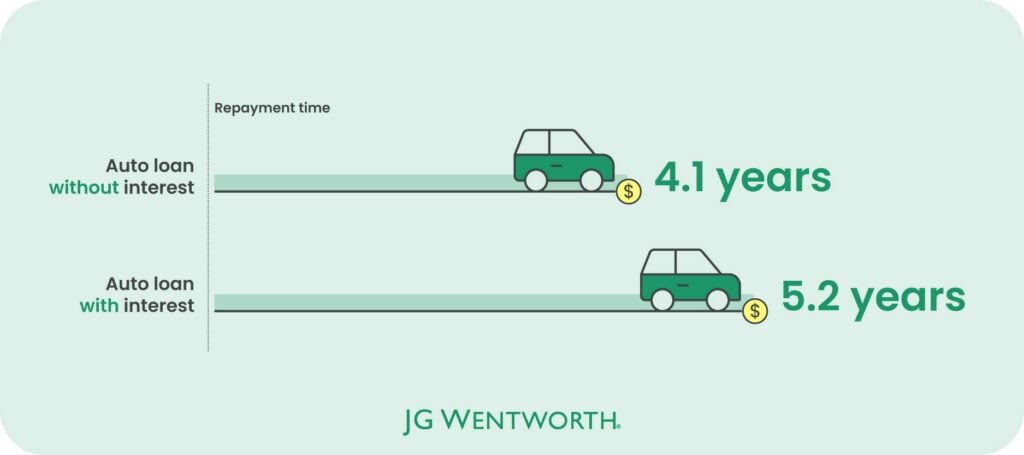

Auto loans can take over 10 years to repay

On average, auto loans take 4.1 years to repay, excluding interest, according to the survey results. This is based on an average loan amount of $12,464 and monthly repayments of $252. When interest is included, this rises to around 5.2 years, adding approximately 14 months to the timeline.

| Scenario | Repayment Time (Years) |

|---|---|

| Auto loan without interest | 4.1 |

| Auto loan with interest | 5.2 |

More than two in five respondents (42.8%) report paying between $100 and $200 per month on their auto loan, which could extend repayment timeline by approximately 5.2 to 10.4 years, to pay off the average auto loan ($12,464). This highlights how lower monthly repayments can add several years to auto loan timelines.

Student loan repayment lasts nearly twice as long (7.4 years) as completing a degree (4 years)

Among those surveyed, 56.5% currently have a student loan. On average, those students spend almost twice as long paying student debt (7.4 years) as they do studying (4 years for a Bachelor’s Degree). [4]

On average, these loans take 7.4 years to repay, or 5.8 years excluding interest, based on an average balance of $13,400 and monthly repayments of $191.

Nearly half of respondents (47.7%) pay between $101 and $200 per month, while a further 10.9% pay just $0-$100 per month. At this lower level, repayment would take approximately 134 months (11.2 years), excluding interest. Minimum monthly payments could extend the repayment period, as payments are applied to outstanding interest before reducing the principal, slowing how quickly the balance is paid down. [5]

Typical student loan repayment timelines can vary widely depending on the repayment plan. According to the Consumer Financial Protection Bureau, standard payment plans are designed to be paid off in 10 years, while income-driven plans can extend repayment to 20 to 25 years. [6]

Credit card debt takes the least time to pay off

Among those surveyed, credit card debt takes 1.3 years to repay on average, excluding interest. However, 11.5% of respondents pay up to $100 per month, and at these lower repayment levels, timelines could extend to four to eight years or more.

But debt can last longer as balances are often carried month to month. Less than half (47%) of U.S. credit cardholders carry a balance, and 22% say they may never fully pay it off, [7] highlighting how lower repayment amounts can significantly extend time in debt.

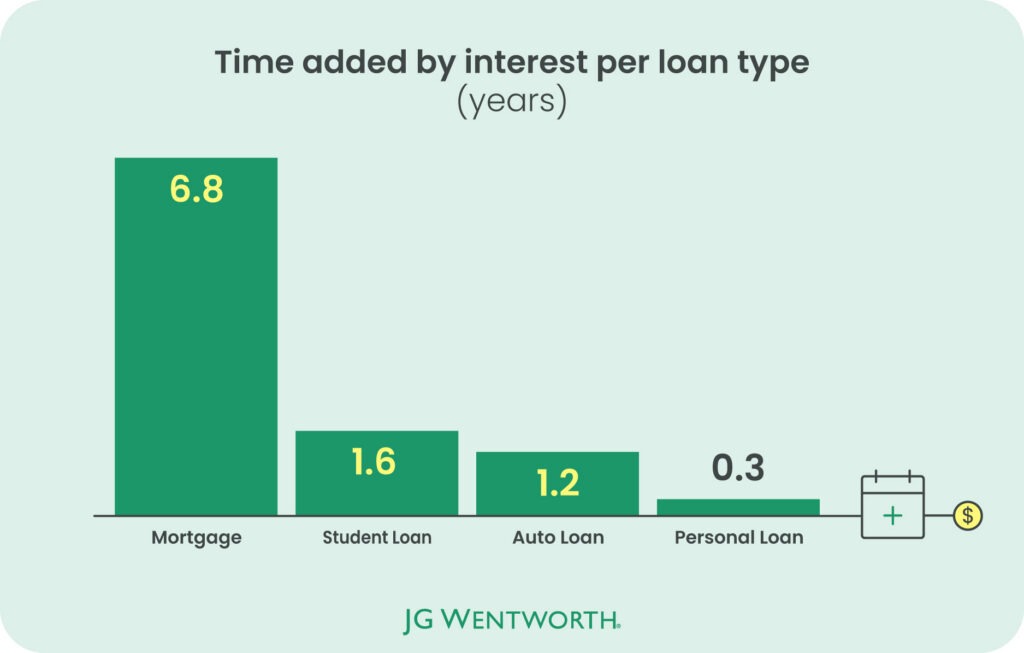

Interest can cost borrowers up to six and a half years

We calculated how long loans take to repay without interest, but in reality, a portion of each payment is applied to interest before reducing the balance. This slows down how quickly balances fall and extends repayment timelines.

Survey results show that interest does not just increase cost, it also adds a significant number of months to the term. In some cases, this is substantial, with mortgage interest adding 6.8 years to the average repayment timeline.

| Loan Type | Time Added (Years) |

|---|---|

| Mortgage | 6.8 |

| Student Loan | 1.6 |

| Auto Loan | 1.2 |

| Personal Loan | 0.3 |

Mortgage interest adds more than six years to repayments on average

Mortgages are amortized, so monthly payments stay the same, but early payments are weighted more heavily toward interest because it is calculated on the remaining balance. [8] As the balance falls, more of each payment goes toward the principal.

Respondents would take an average of 10.7 years to repay their mortgage, excluding interest, rising to 17.5 years when interest is included. This adds 6.8 years, meaning interest alone extends the repayment timeline by nearly seven years.

Interest adds over a year of repayments on some loans

Interest adds over a year of repayments to some loans, extending timelines by months or even years, depending on the type of borrowing.

On average, student loan repayment increases from 5.8 years to 7.4 years, adding 1.6 years. Auto loans rise from 4.1 years to 5.2 years, adding 1.2 years, while personal loans increase from 2.1 years to 2.4 years, adding 0.3 years.

What type of borrowers stay in debt the longest?

Across the survey, the length of time spent in debt is driven more by the amount borrowed and monthly repayments.

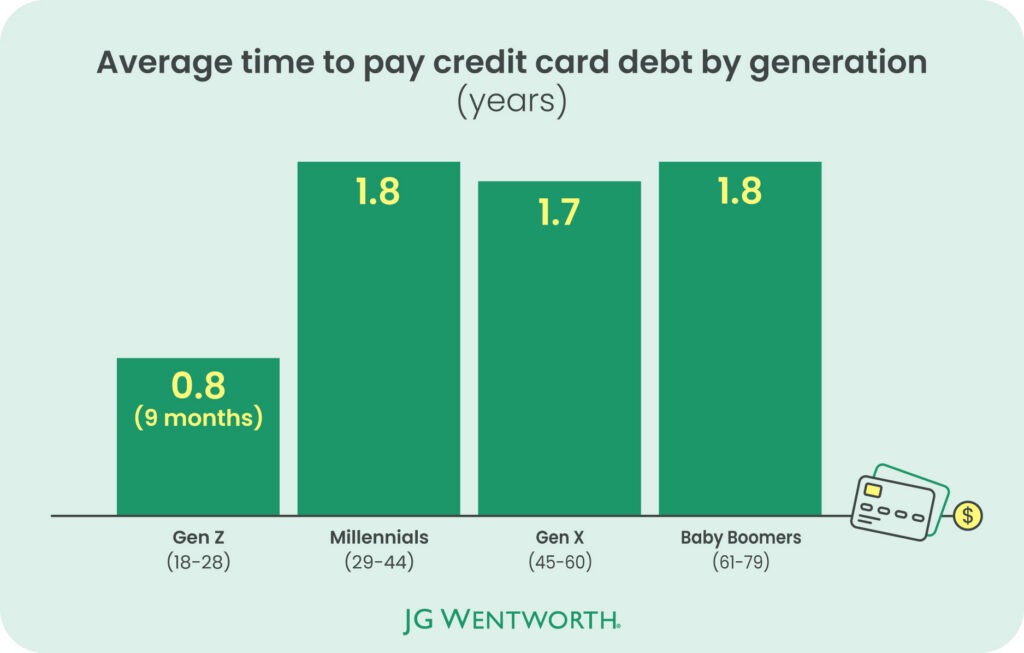

Gen Z pay their credit card debt off the quickest (within 9 months)

On average Gen Z repay their credit card debt in 9 months, while older groups (Gen X and Baby Boomers) repay in 1.8 years (22 months). The balance amounts could explain why there’s a discrepancy between the time it takes to pay off, with older borrowers having larger outstanding balances, with average debt nearly four times as high, at $6,327, compared to $1,652.

While the younger generation takes less than a year to settle their credit card debt, Millennials, Gen X, and Baby Boomers all take a similar time to pay off their debts, paying over 1.8, 1.7, and 1.8 years, respectively.

| Generation | Repayment Time (Years) |

|---|---|

| Gen Z (18–28) | 0.8 (9 months) |

| Millennials (29–44) | 1.8 |

| Gen X (45–60) | 1.7 |

| Baby Boomers (61–79) | 1.8 |

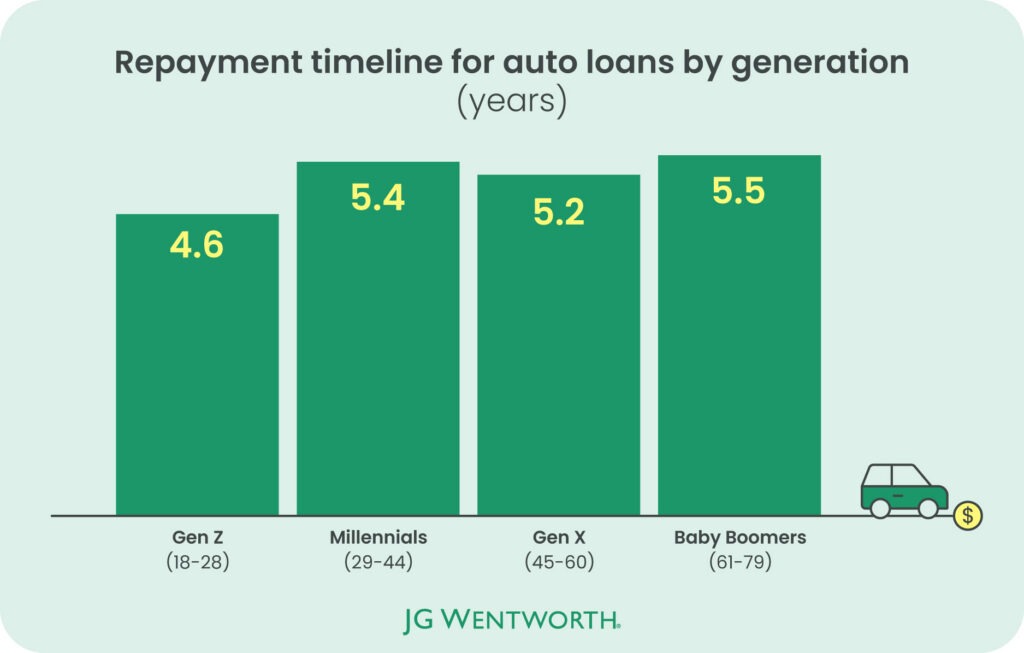

Gen Z pay their auto loans off quicker than all other generations

Despite being allowed on the road for the least amount of time, Gen Z are the quickest generation to pay off their auto loans, taking less than five years (4.6) on average compared to 5.5 years that it takes Baby Boomers, 5.4 for Millennials, and 5.2 for Gen X.

Older generations report average auto loan balances of $17,812, more than double the $8,673 held by Gen Z, which contributes to longer repayment timelines despite similar repayment behavior.

| Generation | Repayment time (years) |

|---|---|

| Gen Z (18–28) | 4.6 |

| Millennials (29–44) | 5.4 |

| Gen X (45–60) | 5.2 |

| Baby Boomers (61–79) | 5.5 |

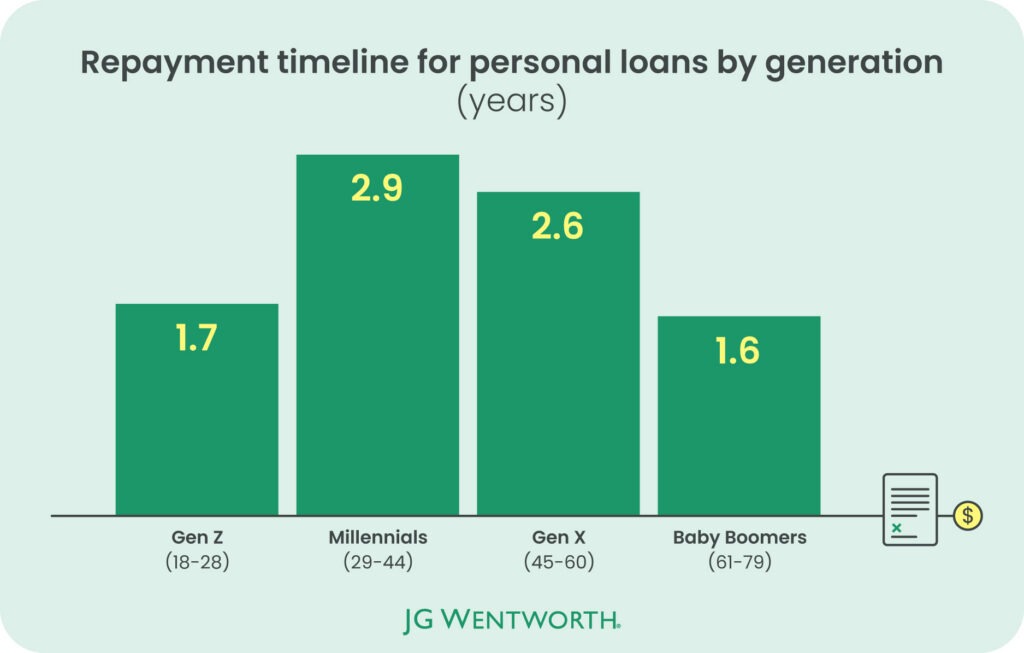

Millennials take around 80% longer to repay personal loans than Baby Boomers

Millennials take significantly longer than Baby Boomers and Gen Z to pay off their personal loans, repaying over 2.9 years compared to 1.6 and 1.7 years.

Baby Boomers pay off their personal loans quicker than all of the other generations, followed closely by Gen Z. Gen X pays off their debt slightly faster than Millennials, taking 2.6 years on average.

This pattern aligns with borrowing levels, with Millennials and Gen X carrying larger average balances of $9,277 and $9,988, compared to $4,958 for Gen Z and $5,556 for Baby Boomers.

| Generation | Repayment time (years) |

|---|---|

| Gen Z (18–28) | 1.7 |

| Millennials (29–44) | 2.9 |

| Gen X (45–60) | 2.6 |

| Baby Boomers (61–79) | 1.6 |

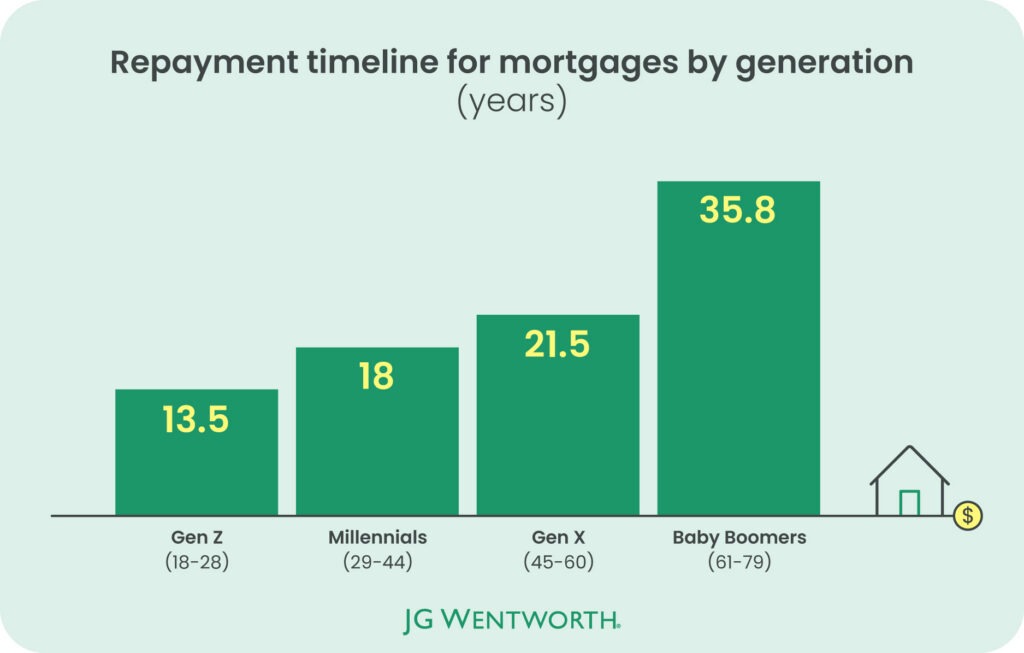

On average, Gen Z borrowers could repay their mortgage in just 13.5 years

Mortgage repayment timelines increase significantly across age groups, with older borrowers taking far longer to clear their loans.

Gen Z repay mortgages in 13.5 years on average, compared to 18 years for Millennials, 21.5 years for Gen X, and 35.8 years for Baby Boomers, showing how repayment length can extend well into later life.

| Generation | Repayment time (years) |

|---|---|

| Gen Z (18–28) | 13.5 |

| Millennials (29–44) | 18 |

| Gen X (45–60) | 21.5 |

| Baby Boomers (61–79) | 35.8 |

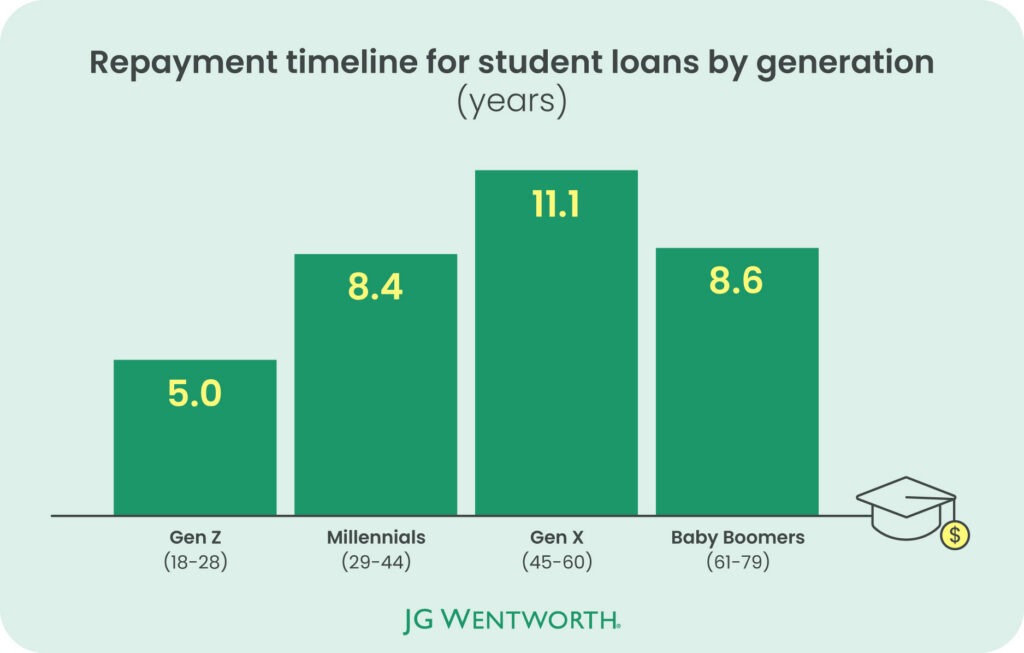

Student loan repayment timeline more than doubles from Gen Z to Gen X

Gen X takes over twice as long to repay their student loans as Gen Z, taking 11.1 years compared to 5.0 years.

This difference aligns with borrowing levels: Gen X carries average balances of $22,073, compared to $9,703 for Gen Z. Higher loan amounts could increase total interest paid over time, which may extend repayment timelines.

| Generation | Repayment time (years) |

|---|---|

| Gen Z (18–28) | 5 |

| Millennials (29–44) | 8.4 |

| Gen X (45–60) | 11.1 |

| Baby Boomers (61–79) | 8.6 |

Borrowers without children stay in debt longer across most loan types

| Generation | Repayment time (years) |

|---|---|

| Gen Z (18–28) | 13.5 |

| Millennials (29–44) | 18 |

| Gen X (45–60) | 21.5 |

| Baby Boomers (61–79) | 35.8 |

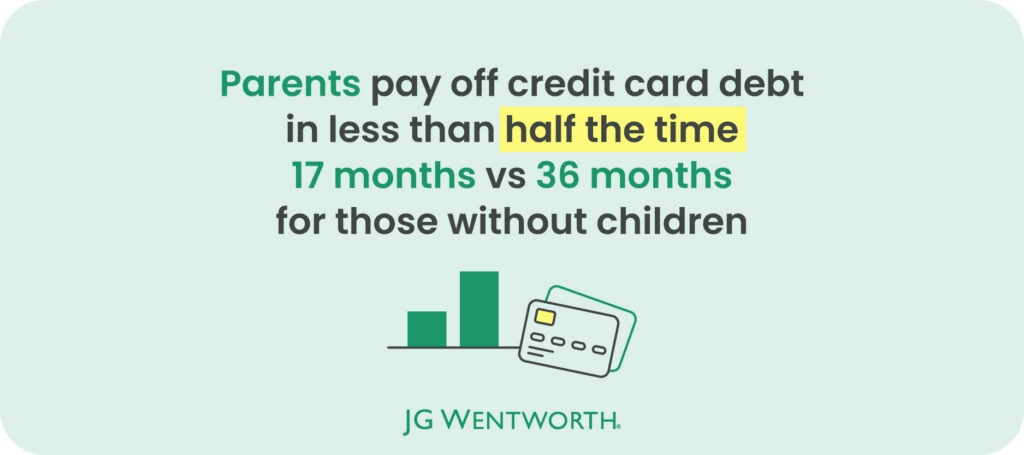

Respondents with children pay off their debts significantly faster than those without, across all types of loans, with the biggest difference (6.6 years) being how long it takes to settle a student loan, with it taking parents 7.2 years compared to 13.8 years for those without children.

Other loans followed the same pattern, with parents paying personal loans faster, in just 24 months compared to 5.9 years, a 3.9 year-difference. Credit card balances are settled in less than half the time (17 months vs 36 months).

Those surveyed with children will finish paying their mortgage three years (36 months) before those without, taking 17.2 years compared to 20.2 years.

Methodology

The survey was conducted in March 2026 and asked 1,376 U.S. adults about their debt, loan balances and monthly repayments amounts.

For some questions, respondents were able to select multiple answers, so totals may not add up to 100%.

The demographics of the survey respondents were:

Gender:

- Female – 78.1%

- Male – 19.5%

- Non-binary – 1.7%

- Not listed – 0.4%

- Prefer not to say – 0.3%

Age:

- 18–28 – 22.8%

- 29–44 – 63.0%

- 45–60 – 12.4%

- 61–79 – 1.7%

Interest rates were sourced from a combination of national benchmarks and industry data to reflect typical borrowing conditions across loan types. Average rates were taken from Experian for auto and personal loans, the Federal Reserve Bank of St. Louis (FRED) for 30-year mortgage rates, and recent estimates reported by CNBC for federal student loan interest rates.

These rates were applied to average loan balances and monthly repayments from the survey to estimate repayment timelines with interest, allowing for a consistent comparison across different types of debt.

Sources

- Consumer debt levels and breakdown:

Experian, Consumer Debt Study. https://www.experian.com/blogs/ask-experian/research/consumer-debt-study/ - U.S. household debt distribution:

Federal Reserve, Survey of Consumer Finances 2023. https://www.federalreserve.gov/publications/files/scf23.pdf - 30-year mortgage rate data:

Federal Reserve Bank of St. Louis, 30-Year Fixed Rate Mortgage Average in the United States. https://fred.stlouisfed.org/series/MORTGAGE30US - Southern New Hampshire University. “How Long Does It Take to Get a Bachelor’s Degree?” https://www.snhu.edu/about-us/newsroom/education/how-long-does-it-take-to-get-a-bachelors-degree

- Student loan payment structure and interest application:

Edfinancial, Payments, Interest, and Fees. https://edfinancial.studentaid.gov/payments-interest-and-fees - Student loan repayment timelines:

Consumer Financial Protection Bureau, How long does it take to pay off a student loan? https://www.consumerfinance.gov/ask-cfpb/how-long-does-it-take-to-pay-off-a-student-loan-en-621/ - Credit card debt trends and repayment behaviour:

Bankrate, Credit Card Debt Report. https://www.bankrate.com/credit-cards/news/credit-card-debt-report - Cost of borrowing and interest impact:

U.S. Bank, Understanding the True Cost of Borrowing. https://www.usbank.com/financialiq/manage-your-household/manage-debt/understanding-the-true-cost-of-borrowing.html

About the author